Business Mobile Subscriptions to Outgrow Consumer Segment in Western Europe

Brexit Could Hinder Growth in the UK

CCS Insight recently published its latest market forecast for cellular business subscriptions in the five biggest European markets of France, Germany, Italy, Spain and the United Kingdom. It covers the mobile subscriptions attributable to business clients, including small companies of up to 10 employees and enterprises of more than 10 employees, and excluding machine-to-machine connections.

Given the mature nature of the consumer segment, businesses are becoming increasingly important to mobile operators. This is particularly relevant as operators look to offer converged services to an increasingly mobile workforce. However, business subscriptions data is inconsistently reported by the market and by operators, and it’s specifically scarce about small businesses that subscribe to mobile services on consumer tariffs. Therefore, we have made significant efforts to place all data on the same consistent level, estimating all missing pieces of the puzzle through our extensive research. Below are some key findings.

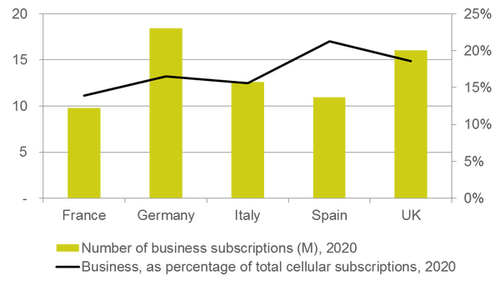

Spain and the UK lead the way for share of business subscriptions in the total mobile subscriptions market. In Spain, 21 percent of all cellular subscriptions are currently billed and used by businesses. Small companies represent a relatively large proportion of business subscriptions — more than a third — because of the great number of such enterprises active in Spain. The UK is not far behind; with 16 million subscriptions, businesses account for 19 percent of all mobile connections. Of those, just over a quarter are small companies, on business or consumer tariffs. Home of many big corporations, the UK sees the other three quarters of business subscriptions billed to larger enterprises.

Generally, we expect that in the next four years, business subscriptions will outgrow the consumer segment in the five covered markets. CCS Insight forecasts Germany and France to see the strongest percentage growth. With an estimated share of business subscriptions of 13 percent in France and 15 percent in Germany, it’s clear that the business market in these countries is underpenetrated compared with the UK and Spain.

In Italy, businesses also account for about 15 percent of mobile subscriptions. Somewhat counter-intuitive, this share will increase in the face of weak macroeconomic growth in Italy, as consumer subscriptions continue to drop and consumers reduce the number of SIMs per head — a very high number in Italy. For example, Vodafone alone has seen a fall of over 2.5 million subscriptions in the last two years. Another reason why Italy stands out from the crowd is the relatively large share of prepaid subscriptions within the business segment. In fact, the vast majority of contract mobile customers in Italy are companies.

In the UK, the implications of Brexit are hard to skip. We expect macroeconomic uncertainty and low macroeconomic growth between 2017 and 2019 to have a negative effect (see Brexit’s Far-Reaching Impact on UK Operators). Business subscriptions will not suffer a massive hit as mobile communications will remain a major tool for companies. However, assuming the weaker pound leads to price rises and lower consumer confidence, some small companies may feel the crunch. Furthermore, we expect businesses to become more cautious in investing and hiring for the next two years. Therefore, of the five markets covered by our forecast, we expect the UK to see the lowest growth of business mobile subscriptions over the next five years.

For further information about CCS Insight’s forecast for business mobile subscriptions, please contact info@ccsinsight.com.

LinkedIn

LinkedIn

Email

Email

Facebook

Facebook

X

X