Recovery Lessons from China

Creating a view of technology markets after the pandemic

How the global technology sector recovers from the unusual crisis caused by the Covid-19 pandemic is a major question we face right now, and it’s something I’ve been thinking about in my role leading the FDM CCS Insight forecasting team. China, which went into a lockdown in late January and gradually emerged from it in March, two to three months before other major economies, provides some big clues that can help map out the recovery in other countries.

Importantly, some of the numbers from China in the first three months of 2020, showing decline in demand for products like mobile phones, have proven to be a good benchmark for the fall in demand in many other markets around the globe in late March to May.

So, let’s look at how mobile phones, mobile subscriptions and 5G, and e-commerce have fared in China since the lifting of the lockdown and the return to a somewhat normal economic life.

Mobile Phones

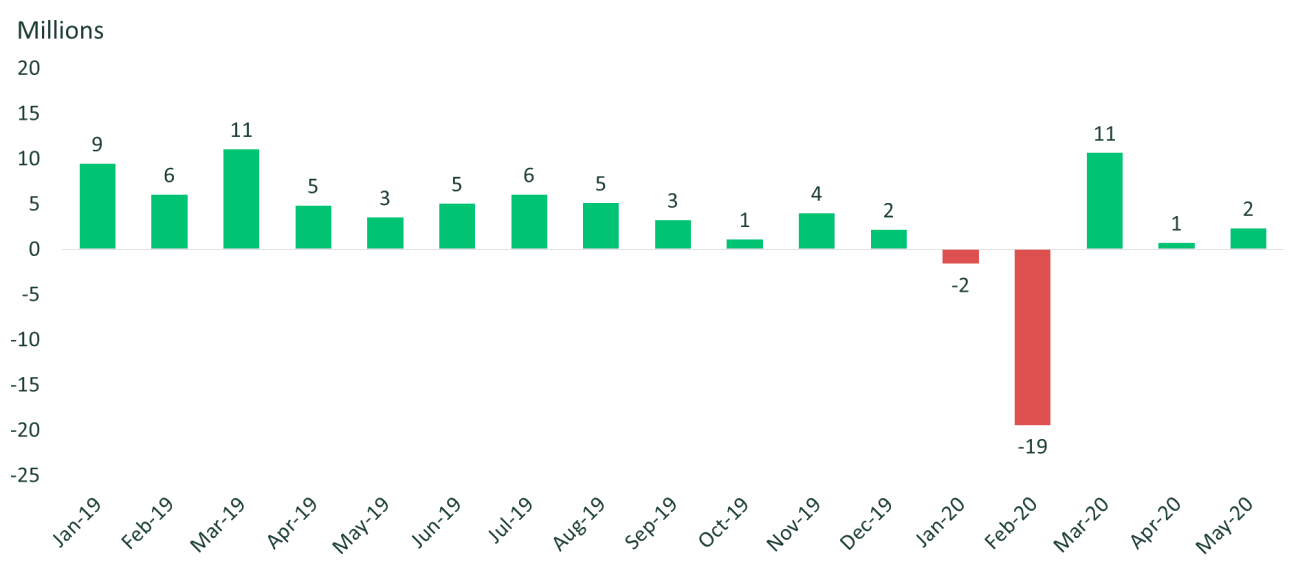

Domestic shipments of mobile phones in China shrank by 36% in the first quarter of 2020. Disruption to the manufacturing and distribution of products played a role, but the real problem was weak demand.

In early April, however, good news arrived from China when several large technology players enthusiastically reported that sales had bounced back in the last couple of weeks of March and the first weeks of April. Clearly there was some pent-up demand, delayed from the first quarter, and shipments in April rose 14% from a strong April 2019.

But this positive development was short-lived: in May sales wilted again, this time by 12%. Overall, for the first five months of 2020, Chinese domestic mobile phone shipments dropped 18% from the same period of 2019 (see Figure 1 below).

Figure 1. Domestic mobile phone shipments in China, year-on-year growth

The reason for this sustained weakness in demand for mobile phones lies in low consumer confidence and loss of income in the face of a weak global macroeconomic outlook. As most of the world went into lockdown, Chinese exports fell 3.3% year-on-year in May, and domestic retail sales in China slipped 2.8% (although this was a significant improvement from April).

As many countries lift their lockdowns and resume wider economic activity, we expect their mobile phone markets to follow a similar pattern of recovery as we’ve seen in China.

Mobile Services

Interestingly, the number of mobile subscriptions in China also tumbled in January and February. It was a small decline compared with the total market of 1.583 billion connections at the start on 2020, but it was unusual, as connections have been growing consistently for quite some time. The best explanation probably reflects the lower economic activity in those two months. It’s likely that some companies disconnected lines they didn’t need during lockdown, especially as they weren’t sure when their businesses would be allowed to reopen. The number of subscriptions started to grow again in March but hasn’t yet bounced back to the levels seen in December 2019.

Despite the difficult macroeconomic situation, no further decline in mobile subscriptions has been recorded since February. It seems that people and companies are prioritizing mobile connectivity even in difficult times, as it’s a crucial way to stay in business.

Figure 2. Mobile subscriptions in China, net additions

E-Commerce

Although consumer confidence in China is low, and businesses are reeling from weak domestic and international demand, one trend is going from strength to strength: the shift to online shopping. This, coupled with an appetite for good deals, led to great results at the recent 618 online shopping event. Created by e-commerce giant JD.com, this annual event lasts for about three weeks and ends around 18 June.

The success of the event is clear from the volume of transactions on JD.com, which reached 269 billion yuan ($38 billion), up 34% over the year. Alibaba reportedly saw transaction volumes of 698 billion yuan ($99 billion). We don’t have an exact year-on-year comparison for this number, but Alibaba revealed that in the first 10 hours of the event, transaction volume was up more than 50% over the year. We’ll discuss the recent 618 shopping event in more detail in an upcoming blog post.

Chinese consumers may be shopping less, but they’re spending a growing portion of their money online, even when bricks-and-mortar shops are open.

What Can Other Markets Learn from Post-Lockdown China?

Consumer demand for technology products is unlikely to recover overnight. We might see initial spikes in demand when shops open, but the next few months will be plagued by macroeconomic uncertainty and low consumer confidence, and so we expect sales of gadgets will take time to bounce back. Mobile services, however, are much more resilient.

Although shops are now open in many countries, retailers should continue to nurture their online business, as we expect that the shift to more online shopping is here to stay.