Extended Reality Sails Toward Better Times

- Supply constraints limited growth in the markets for virtual and augmented reality devices in 2020, despite strong demand — but the outlook is positive

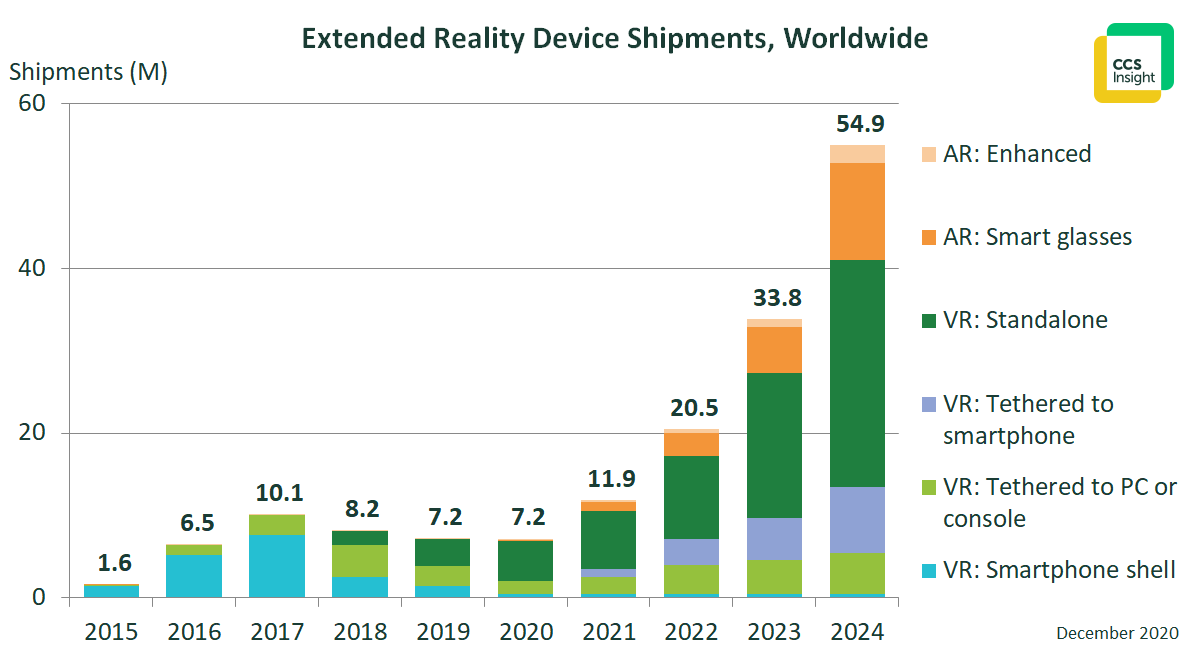

- FDM CCS Insight forecasts that 55 million virtual and augmented reality devices will be sold in 2024, with a market value of $14.7 billion

- Future growth will be helped by uptake of innovative, more compact smart glasses supported by 5G smartphones

8 December 2020, London: Disrupted supplies in the first half of 2020 and economic softness in the second half took their toll on the market for extended reality devices, but consumer excitement about new products and strong interest from enterprises are paving the way for solid adoption of these devices in the future, according to technology market analyst firm FDM CCS Insight. Its latest market forecast projects sales of virtual and augmented reality (VR and AR) devices to fall 1% in 2020 to 7.2 million units, but to grow strongly over the next four years to reach 55 million units in 2024.

“An almost flat market is a good result in this extraordinary year,” comments Marina Koytcheva, Vice President of Forecasting at FDM CCS Insight. “To put things in perspective, the largest consumer electronics category in the world, mobile phones, will see a decline of 15% in 2020, following the disruption caused by the Covid-19 pandemic.”

“Sales of VR and AR devices, to both consumers and enterprises, would have been higher if some of the main players had been able to ramp up production faster,” explains Leo Gebbie, Senior Analyst for Extended Reality at FDM CCS Insight. “Facebook suffered shortages of the original Oculus Quest earlier in the year, and in the autumn we saw huge numbers of pre-orders for the attractively priced Oculus Quest 2. This demand shows the potential of standalone VR headsets, which will form half of all extended reality device sales in 2024.”

This year has presented other obstacles for the market. The launch of the new Xbox Series X and Series S and the new PlayStation 5 dented interest in VR devices, as many gaming enthusiasts directed their Christmas spending toward a new console rather than a VR headset. FDM CCS Insight expects VR devices that attach to a PC or games console will become a niche part of the market.

However, recent announcements by Qualcomm at its Snapdragon Tech Summit confirm our view that affordable VR and AR devices that connect to a smartphone are a growth segment. We expect that telecom operators will become a key part of the distribution network for extended reality devices, especially as they seek to position VR and AR headsets as accessories to pair with 5G-capable smartphones.

Meanwhile, the enterprise market witnessed a significant rise in demand for extended reality devices and services in 2020. “This year presented a golden opportunity for the technology to finally make the step from promise to reality in enterprises and educational institutions,” according to Angela Ashenden, Principal Analyst for Workplace Transformation at FDM CCS Insight. Sales of extended reality headsets to the enterprise are expected to swell almost 2.5 times in 2020 to reach 650,000 devices. These products are most often used to provide business continuity in scenarios related to remote field service, manufacturing, product demonstration, training and other areas.

“This year, extended reality companies grew in the enterprise space as much as their production and distribution reach allowed them”, explains Ashenden. Epson, Google, RealWear and Vuzix are among the companies that have benefited from a focus on the enterprise market, thanks to their established distribution and relationships with different industry sectors. Demand for extended reality in enterprises and education is expected to remain strong and more than double again in 2021, despite difficult economic conditions, reaching 8.2 million devices by 2024.

In addition to these positive indicators for the extended reality industry, FDM CCS Insight also highlights signals that support its prediction that consumer AR glasses will emerge as an important category by 2023, including products from major consumer brands like Samsung, Facebook and Apple. This nascent market, comprising just 50,000 devices in 2020, has the potential to reach 9 million units by 2024, should new lightweight stylish devices grab the attention of technology enthusiasts in the next few years.

A summary of FDM CCS Insight’s new forecast is presented in the chart below.

More details of FDM CCS Insight’s extensive VR and AR research service can be found at www.ccsinsight.com/research-areas/virtual-and-augmented-reality

Notes to editors

FDM CCS Insight is a leading provider of research on the extended reality market. Its VR and AR device forecast covers several product segments and presents three scenarios (core, low and high) that plot the effects of different market developments.

This forecast is part of a broader suite of research into extended reality technology, including an extensive database of devices in this area, regular reports and updates on the latest announcements, events and news.

About FDM CCS Insight

FDM CCS Insight is a global analyst company focussing on current and future trends in technology. It provides comprehensive services that are tailored to meet the needs of individual clients, helping them make sense of the connected world. Follow @ccsinsight on Twitter or learn more at www.ccsinsight.com.

For further information contact:

Sophie Adams

Harvard PR

Tel: + 44 (0) 738 502 3639

E-mail: ccsinsight@harvard.co.uk