The Bottleneck Holding Back Satellite Companies

Interest in satellites is at an all-time high. Earlier in June, SpaceX successfully filed for an IPO with a massive $1.77 trillion valuation, making it one of the most-valuable companies on Earth. The main reason for its high valuation is the excitement and opportunity that this space — pun intended — has to offer.

However, SpaceX’s pursuits rely on launch capacity. The same is true for any company that’s eyeing opportunities in this growing market. Companies need to transport their assets from Earth into space. Yet even with all the investment and forecasts of billions in revenue, launch capacity remains a major problem today — for SpaceX, but more significantly, for the wider satellite network industry.

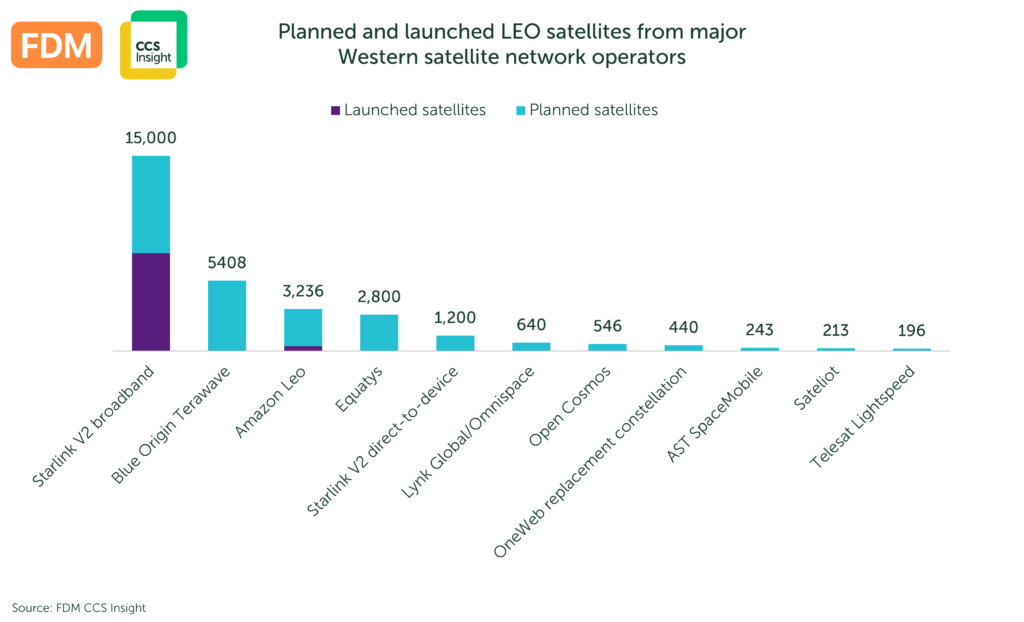

Currently, there are approximately 15,000 low-Earth-orbit (LEO) satellites in orbit, and about 10,000 of them belong to Starlink. The company has launched them using a steady cadence of SpaceX rockets over the past five years or so, most notably the Falcon 9 and the Falcon Heavy.

However, the number of satellites in space today will be a footnote compared with the volume planned by satellite companies. Starlink recently received approval for up to 15,000 V2 satellites for broadband, up 7,500 from its previous quota. Other companies are planning significant launches of LEO satellites to provide broadband or direct-to-device connectivity, as shown in the chart below.

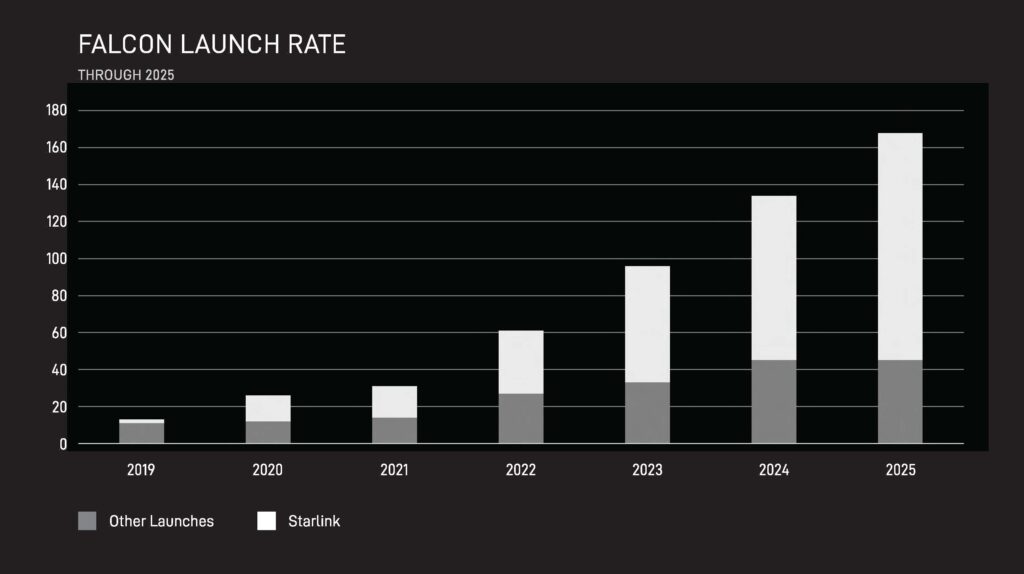

To get these satellites into space, satellite network operators must find a launch partner. As I mentioned above, SpaceX has a couple of rocket vehicles. In its annual report, it said that the number of Falcon rocket launches rose 18% year-on-year in 2025 to 170, shown below. This sounds encouraging, but the number of launches containing non-Starlink payloads remained largely unchanged compared with 2024, leaving no additional capacity for competitors.

There are other potential launch partners for satellite operators. Blue Origin is the strongest competitor for relative payload size, but the Jeff Bezos-owned company has suffered a series of setbacks in recent weeks. It failed to deploy an AST SpaceMobile satellite to the correct height, meaning the satellite was de-orbited. Then a major explosion engulfed the launch site in fire, leading to significant damage to the launch pad and several months of further delays while it’s repaired. But the greater, more-lasting damage is to the company’s reputation.

And, as Blue Origin plans to launch its own constellation, its prospects as a launch partner will go the same way as Starlink. In January, it announced its TeraWave constellation, a network of 5,408 satellites that we expect to absorb even more of the scarce launch capacity.

Other rocket companies have launched with greater regularity than Blue Origin in the first half of 2026, with United Launch Alliance launching three times, ArianeSpace six times and RocketLab 11 times. However, when compared with the 70-plus times that SpaceX has launched in the same period, these competitors clearly lack the same scale and SpaceX’s quick, reusable rockets.

The impact of this lack of large-scale, independent launch suppliers is already being felt throughout the industry. Amazon Leo recently won an extension to its satellite roll-out schedule when it became clear it wouldn’t have even half of its proposed V1 satellite constellation launched by July 2026. Even with its financial muscle and connection with Jeff Bezos’s Blue Origin, the company has still only launched 367 of its targeted 1,618 satellites.

AST SpaceMobile, a US-based satellite supplier that targets the direct-to-device market, has also had a slow roll-out programme so far, even before the Blue Origin mishap. It only launched one satellite in 2025 and just four further satellites deployed in 2026. The company plans to introduce a service at the end of 2026, which still seems optimistic given the limited launch availability. It’s helped, however, by its strategy of pursuing a constellation with fewer, larger satellites.

OpenCosmos, a small UK-based satellite company, is also struggling with the bottleneck. The company missed its deadline of 10 June to launch 144 LEO satellites. It has been granted an extension until September, although this’ll still be a challenge.

Launch capacity is also impacting SpaceX itself. Its current plan is unlikely to be achievable with Falcon 9 and Falcon Heavy alone. SpaceX is dependent on the development of its next-generation launch vehicle, called Starship, which will increase LEO payload capacity by four-to-six times and has been in testing since 2023. In its pre-IPO filing, the company said that if the Starship rocket failed as a project or was significantly delayed, the deployment schedule for its V2 direct-to-device constellation would be affected.

Even with the advancements in rocket technology, the issue of demand outstripping supply is only going to worsen. Several companies are starting to look beyond traditional satellite uses for connectivity and observation. SpaceX, for instance, has filed an application to launch 1 million satellites into orbit to serve as orbital data centres. As we noted when SpaceX merged with xAI, this would require 14 Starship launches per day for 365 consecutive days. Blue Origin submitted an application for 51,600 orbital AI data centres, and Space Cowboy recently filed for 20,000. There’s an argument that all these filings are just “paper satellites” used as a regulatory manoeuvre to reserve orbital plans. However, even a fraction would demand a big increase in launch capacity.

In the short term, we expect very little to change in terms of launch capacity, with the industry struggling to meet the excess demand. Regulators do appear to be accommodating, as seen in the US with Amazon Leo and in Lichtenstein with Open Cosmos.

However, this doesn’t change the fundamentals of the market. To avoid abuses of power, competition watchdogs must provide strong guidance to companies like SpaceX and Blue Origin about how much launch capacity should be offered to unaffiliated satellite constellations. Smaller rocket-makers also need greater investment to increase the size of assets that their rockets can launch, as well as the number of launches each year. The success of SpaceX’s IPO should mean that these small players now receive more love from investors.

The space race is on, and the excitement and intrigue are set to continue.