Bundling Connectivity Up

Forecast Notes Steady Progress in Multiplay Adoption in the UK

CCS Insight has recently published its forecast of multiplay services in the UK. If you’d like more information about the forecast or our Multiplay Strategies research service, please contact us.

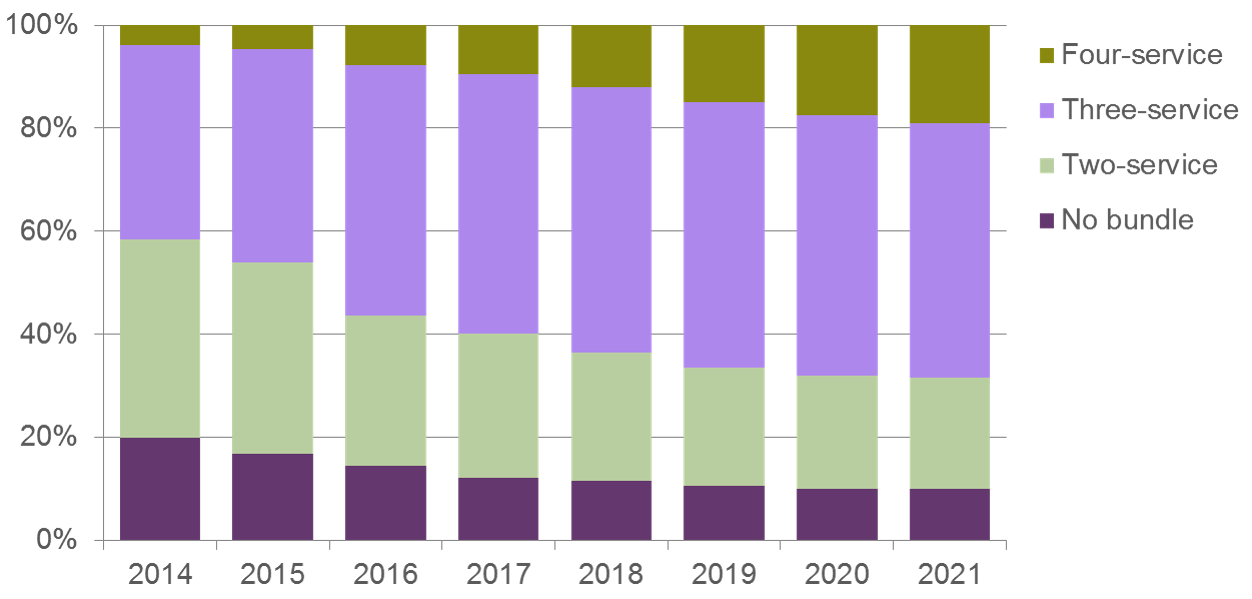

One in 10 UK households will be buying their mobile services, broadband, pay-TV and fixed telephony all from the same provider by the end of 2017. This is double the number from the end of 2015. The number will double yet again by 2021.

Split of households by bundle uptake

The implementation of multiplay strategies by BT and Sky has resulted in all major broadband providers in the UK now offering mobile services. For BT, mobile services are a core product — the EE business contributed 21 percent of BT’s revenue in the final three months of 2016. Sky, on the other hand, appears to be a reluctant participant in the mobile market, although we believe this will change. Despite these differences, it’s clear that both companies will prompt further convergence in the UK’s telecom landscape.

Adoption of multiplay services grew relatively strongly during 2016, partly thanks to BT’s acquisition of EE. However, the rise was not as vigorous as we expected. Sky was late with its launch of mobile services, and BT did not translate ownership of sports rights into subscriptions for its TV channels as fast as we expected. Still, these are short-term delays. Increases in broadband and pay-TV subscriptions in 2016 were good: CCS Insight estimates that 84 percent of UK households subscribe to broadband services, and 56 percent watch pay-TV. This is a good audience for cross-selling more services.

In the next couple of years, we expect competition between the main rivals — BT, Sky, Virgin Media and TalkTalk — to intensify. Strategies will be improved, marketing will be refined and households are likely to be spoiled for choice when selecting a bundle of services. We’re upbeat about the demand for bundles, whether households are looking for convenience or value, and we expect around seven in every 10 households to subscribe to at least three services from the same provider by 2021.

This leaves two big questions. The first is whether pure-play mobile operators like O2 and Three can sustain their positions in the long term. The second is what else converged operators can add to their portfolios to create bundles of five, six or even more services. Connected home and connected cars are definitely contenders.

LinkedIn

LinkedIn

Email

Email

Facebook

Facebook

X

X