Time Running Out for 4G Premiums

Surcharge in UK Could Be Gone by Summer as Tesco Follows 3 to Offer 4G for “Free”

The price premium for 4G services in the UK came a step closer to extinction last week. In a disruptive move, virtual network provider Tesco Mobile confirmed that it will no longer charge an additional £2.50 access fee. This means that all new and existing Tesco Mobile customers now receive 4G for “free”.

The announcement reflects an increasingly competitive UK 4G market. Tesco’s entry SIM-only tariff with a 12-month contract costs just £7.50 per month and includes 500 MB of 4G data – plenty for many consumers. Its 4G smartphone deals begin at an attractive £12.50 per month for the Nokia Lumia 920.

Tesco’s move reinforces my view that a short-lived premium for 4G in the UK will have all but evaporated by the summer. I expect to see EE do away with its current £2 premium before too long, and 3 has already bundled 4G into its complete range of tariffs. Mobile contracts will soon no longer distinguish between 3G and 4G access; customers will automatically receive 4G data when they sign up with their provider.

A competitive 4G market is not unique to the UK, however: premiums are also rapidly being eroded across Europe. France in particular is seeing brutal competition following the move by Free Mobile to offer 4G without extra charge in its flagship €20-a-month tariff. This prompted rivals to respond by also bundling 4G into their plans.

Last week, leading Belgian operator Proximus extended 4G availability to all customers without extra charge. In Spain, the harsh economic climate quickly forced all operators to abandon initial hopes of charging more for 4G. It’s a similar picture in Germany, where leading operator T-Mobile also offers 4G without extra charge.

Tesco’s announcement was bad news for 3, which had been the only UK operator not to charge a 4G premium. Tesco can even boast of wider 4G coverage than 3 given that it piggybacks on O2’s network — O2 currently reaches just over 30% of the UK population compared with the 17% that 3 had reached at the start of the year.

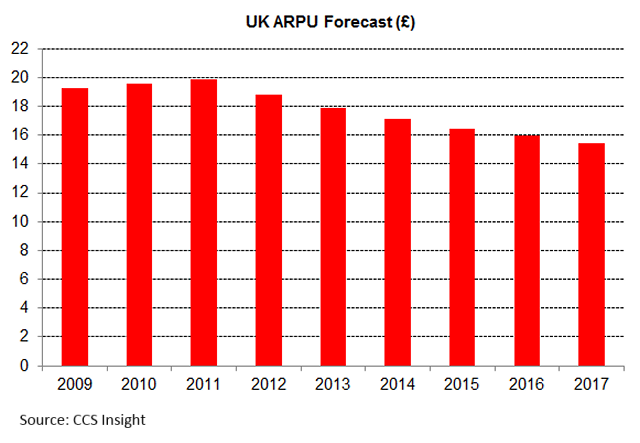

The short lifespan of 4G premiums is a blow to European operators — many had hoped that the premiums would drive extra revenue to fund investment in licences, networks and marketing. Our latest forecast shows that, despite encouraging uptake of 4G in the UK, average overall spend per customer will continue to fall as strong competition keeps prices low (see chart).

This trend confirms my long-held view that the business case for 4G remains unproven. Operators will need to invest in new areas to acquire additional income as they’re unable to sustain higher prices through connectivity alone. It’s unclear where these opportunities lie, but they could include high-growth segments such as M2M, convergence and big data. Operators will need to develop pricing models to support the rapid fall in price of 4G smartphones if 4G prepay tariffs are to thrive. EE has already been offering the Alcatel OneTouch Idol S on prepay for £130, and I expect the first sub-£100 LTE smartphones on prepay plans will arrive before the summer.