Virtual Reality Market Stumbles in 2018

But FDM CCS Insight Forecast Expects It to Bounce Back in 2019

The challenges facing makers of head-worn virtual reality (VR) and augmented reality (AR) devices are underlined in our latest global market forecast. Despite early enthusiasm and a continued expectation of significant long-term potential for the technology, we think there’s still a lot of work to be done to improve the user experience, software platforms and content availability. This sober yet positive message is the main finding of our recently published report, available to FDM CCS Insight clients here.

The challenges facing makers of head-worn virtual reality (VR) and augmented reality (AR) devices are underlined in our latest global market forecast. Despite early enthusiasm and a continued expectation of significant long-term potential for the technology, we think there’s still a lot of work to be done to improve the user experience, software platforms and content availability. This sober yet positive message is the main finding of our recently published report, available to FDM CCS Insight clients here.

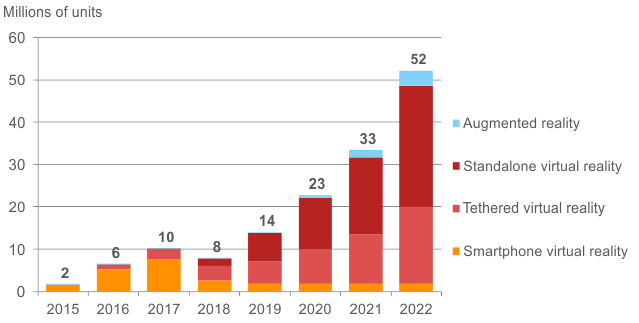

We expect that slightly less than 8 million AR and VR devices will be sold in 2018, growing to 14 million in 2019 and to 52 million in 2022. We continue to believe that content is the key to unlocking adoption of VR, and although some games companies and adult content creators have embraced the technology, much more needs to happen to persuade consumers that VR devices are a must-have item.

The market for VR has gone through several phases. The first wave of consumers used basic cardboard viewers, which helped them understand the potential of the media, but these products offered a limited experience and most people quickly lost interest. Attention then turned to smartphone-based devices like the Samsung Gear VR and the Zeiss One Plus VR. These devices have played an important role in raising the awareness of the technology over the past three years, but interest in these devices has now waned as well.

This is reflected in FDM CCS Insight’s forecast, which shows a dramatic drop in sales of smartphone VR devices, from close to 8 million units in 2017 to fewer than 3 million this year. This steep decline has happened even though the past 12 months have seen heavy price cuts and extensive promotions.

The device market appears to have moved on from the early days of cheaper, less-functional cardboard and plastic smartphone VR viewers, and we expect the next wave of adoption to come from dedicated devices that offer a more compelling, wire-free experience. Interestingly, we don’t even include cardboard products in our forecast anymore.

The advent of standalone VR headsets is expected to help reinvigorate the product category. All-in-one devices overcome the inconvenience of being attached to a PC, smartphone or games console, and so deliver a better VR experience. Headsets such as Facebook’s Oculus Go and Oculus Quest, which are being offered at a retail prices of $200 and $400 respectively, are good examples of the future of VR. The Chinese market is looking particularly promising and Facebook’s partnership with Xiaomi has certainly helped standalone VR headsets make a strong start in China.

We expect standalone devices to be the main driving force for VR adoption in the next few years by both consumers and businesses, with demand growing over 16 times between 2018 and 2022 when 29 million standalone VR headsets are projected to be sold.

While there’s a lot of excitement about standalone devices, we still believe tethered devices like the Sony PlayStation VR, HTC Vive or Oculus Rift will remain an important part of the market, especially as they become wireless. These devices, which need additional computing equipment or a games console, are able to meet the needs of the most dedicated gamers who want a best-in-class experience. Sony, which we consider as the most successful manufacturer of tethered VR headsets to date, looks set to continue with its strategy of offering its VR headset as an accessory to the large number of PlayStation owners. We forecast that 5 million tethered VR headsets will be sold in 2019, rising to 18 million in 2022.

FDM CCS Insight’s latest forecast also looks at the market for AR smart glasses. These have seen significantly slower adoption than their VR cousins, but interest remains high. The main use for these devices continues to be in business operations such as customer service, logistics, remote servicing, design and other related applications.

Businesses have taken a cautious approach to AR devices, initially focusing on pilot deployments, but we’re seeing a rising number of companies committing to deployments of tens or hundreds of AR glasses as they start to see the clear benefits of head-worn technology in the workplace. However, despite this building momentum we still think it will take time for the AR device market to grow. We don’t expect cumulative sales to exceed 1 million worldwide before 2021.

When thinking about AR glasses for consumers, these devices continue to be more common in science fiction than in real life, with little evidence of a product with mass-market appeal any time soon. Nevertheless, our long-range forecast does include a scenario of accelerated adoption if a major consumer brand like Apple decides to enter the market.

The chart below offers a snapshot of FDM CCS Insight’s global forecast of unit shipments of AR and VR devices.

Shipments of VR and AR devices, worldwide, 2015-2022

Source: FDM CCS Insight VR and AR forecast (November 2018)

More details of FDM CCS Insight’s extensive VR and AR research service can be found here.