Sales of Second-Hand Smartphones Continue to Outperform New Devices

- The latest data from FDM CCS Insight shows that the global secondary organized smartphone market enjoyed 7% growth in shipments year-on-year for 2Q24, fuelled by strong consumer demand.

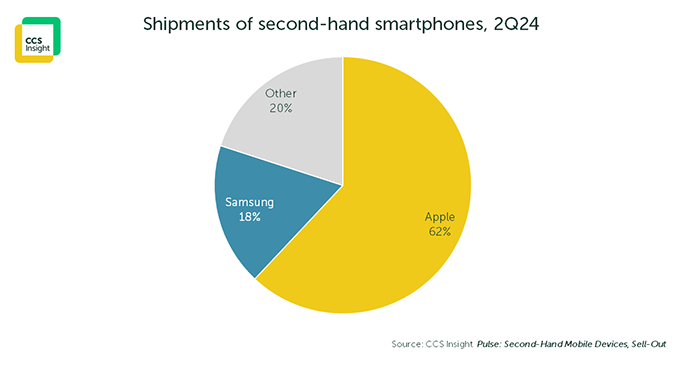

- Apple remains the dominant brand, with iPhones representing more than half of second-hand devices shipped in the quarter. Samsung follows with less than 20% market share.

- Market value declined by 13% as the average price of second-hand devices dropped, mostly because of the continued popularity of older iPhones.

- European regulation of USB-C support on devices is causing some market uncertainty, threatening to stem the flow of devices into a region that is dependent on imports.

London, 18 September 2024: The latest research from FDM CCS Insight found that the organized second-hand smartphone market enjoyed year-on-year growth of 7% in the second quarter of 2024. The company attributes this rise to ongoing economic recovery in most regions as consumers’ financial situations gradually improve.

The research highlights that Apple remains the dominant brand in the organized secondary market, with an estimated 17 million iPhones shipping in the quarter. This contributed 62% of the overall volume, with particular strength in North America. Samsung was the second-largest brand, performing strongly in Latin America, Europe and the Middle East and Africa.

Although shipments of devices increased, the value of the organized secondary market declined by 13% to $7.7 billion. This is mostly down to the continued popularity of older devices in the model mix such as the iPhone 11, which has seen its price slide rapidly yet still contributes a significant share of shipments.

Leo Gebbie, Principal Analyst and Director, Americas, comments, “Consumer demand for second-hand smartphones is accelerating, with low-cost iPhones remaining the most popular pre-owned devices. Our data confirms this, showing that market volume and value is dominated by Apple products. As a result, shifts in demand for iPhones are the most important factor affecting the market on a quarterly basis”.

Importantly, demand for Apple’s recently unveiled iPhone 16 range has the potential to fuel the upgrade cycle in the primary smartphone market. If so, it will result in a wave of traded-in iPhones reaching the second-hand market and provide a welcome boost to supply, which continues to be one of the biggest challenges facing the market.

Gebbie notes, “The potential for a “supercycle” of iPhone 16 upgrades has been a hot topic in the industry. A mass movement of users to the latest model could result in a flood of iPhone 12, 13 and even 14 devices reaching the organized secondary market. This will depend on whether Apple Intelligence is a big enough draw to truly move the needle in terms of upgrades”.

Another crucial dynamic is the impending Radio Equipment Directive in the EU. Slated for 28 December 2024, the regulation will require all devices to support USB-C, with the intention of reducing e-waste by outlawing proprietary chargers.

This regulation will affect the primary and secondary markets, and FDM CCS Insight estimates that more than 60% of the European second-hand smartphone market will not support USB-C when the ruling comes into force. Although the ban applies only to imported models, FDM CCS Insight predicts that in 2025 this will cut two out of five units from supply, or 8 million smartphones, worth €2 billion in sales.

Simon Bryant, Vice President of Research, explains, “The USB-C mandate will strain the still-emerging circular industry, which has already seen several companies cease trading this year because of tough market conditions. It also risks pushing trading into unregulated channels and is likely to promote parallel imports bypassing EU customs”.

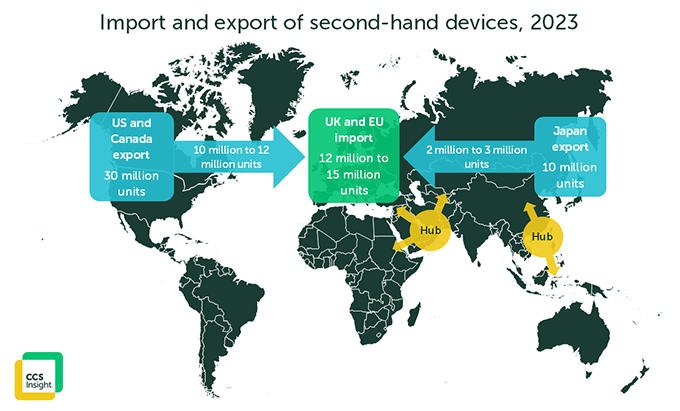

FDM CCS Insight observes that Europe is the greatest importer of used phones, primarily from the US as well as Japan and Singapore. Bryant adds, “This situation demonstrates Europe’s dependence on devices from other regions and, ultimately, the non-circular behaviour of consumers and channels in Europe despite their commitment to sustainability initiatives. The European telecom industry recognizes that it needs to address low trade-in throughout the region, but it’s still far off the pace of the US and Japan, which generate much higher volumes”.

In 2024, FDM CCS Insight expects that sales volumes in the organized secondary market for smartphones will outperform 2023, but with significant variation by region. Notably, year-on-year growth will outpace the market for new devices as consumers continue to see the benefits of purchasing second-hand technology to save money and help the environment.

The latest quarterly update of the market tracker is available now. Contact FDM CCS Insight for more information.

About FDM CCS Insight

FDM CCS Insight’s research and advisory services keep technology companies informed of current and future trends in a range of industries. Its global insights provide technology professionals with clarity and confidence in their decision-making processes.

Follow FDM CCS Insight on LinkedIn to keep up with the latest industry news and research.

For media enquiries contact:

Harvard PR

Email: ccsinsight@harvard.co.uk